Southeast Asian field on track for first gas in 2027

What happened

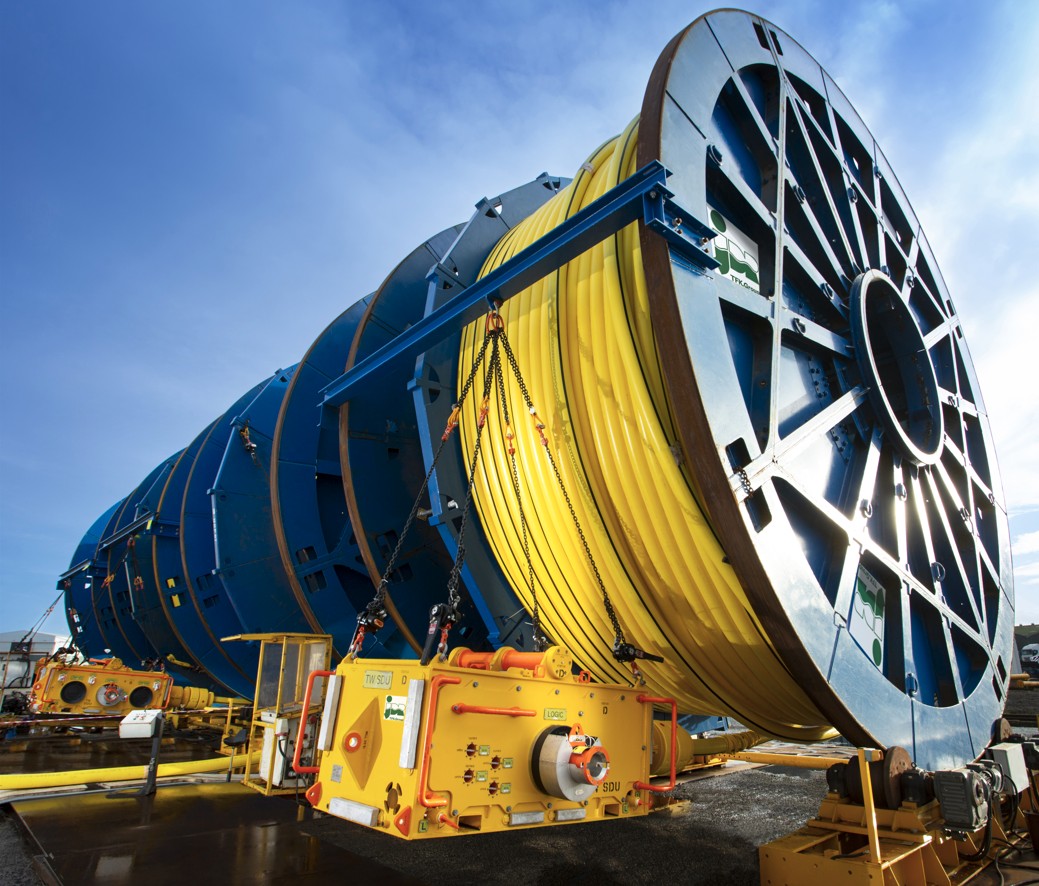

Following a March FID, West Natuna Exploration and partners issued letters of award covering drilling, subsea, SURF, EPCI and long‑lead items for the Mako gas project in Indonesia. The awards and milestone payments cover the majority of capital contracts and keep the project on track for first gas under the current timeline. Watch supplier mobilisation clauses, milestone payment sequencing and local logistics readiness as the next operational signs

Buyer takeaway

Treat this as an operational mobilisation signal that will pull fabrication, SURF and drilling resources—prepare mobilisation and supplier‑leverage strategies now

Cost / money

Milestone payments and concentrated LOAs reduce the buyer’s ability to negotiate mobilisation timing and increase exposure to expedited mobilisation premiums unless contract controls are applied

Supplier / commercial

Concentrated scope awards strengthen incumbents’ negotiating posture and shorten windows to re‑tender, increasing the chance of conditional timing clauses and narrow quote validity

Safety / operations

Compressed execution timelines raise HSE readiness risk—ensure early inductions, camp logistics and permit alignment to avoid execution blockers during mobilisation

What to watch

Monitor contract wording for short quote validity, conditional mobilisation triggers and fuel or expedite pass‑through mechanisms that shift cost risk to the buyer

Key facts

- Letters of award cover more than $280 million of capital contracts (reported)

- Project scope includes drilling, SURF, umbilicals and EPCI long‑lead items

- Sales gas tied via ~59 km pipeline into adjacent infrastructure

Source excerpts

5%) and Coro Energy (15%), set the Mako gas project development activities in motion with letters of award covering more than $280 million of capital contracts, constituting over 80% of the total capital costs. As a result, letters of award have been issued for the drilling rig, subsea, umbilicals, risers, flowlines (SURF), engineering, procurement, construction, and installation (EPCI), conductor support frame (CSF), EPCT, and all long lead items

As a result, letters of award have been issued for the drilling rig, subsea, umbilicals, risers, flowlines (SURF), engineering, procurement, construction, and installation (EPCI), conductor support frame (CSF), EPCT, and all long lead items

As a result, letters of award have been issued for the drilling rig, subsea, umbilicals, risers, flowlines (SURF), engineering, procurement, construction, and installation (EPCI), conductor support frame (CSF), EPCT, and all long lead items. The operator has confirmed that several milestone payments have already been made to the contractors, with costs remaining in line with previous guidance