Europe, Asia LNG prices climb on Hormuz closure

What happened

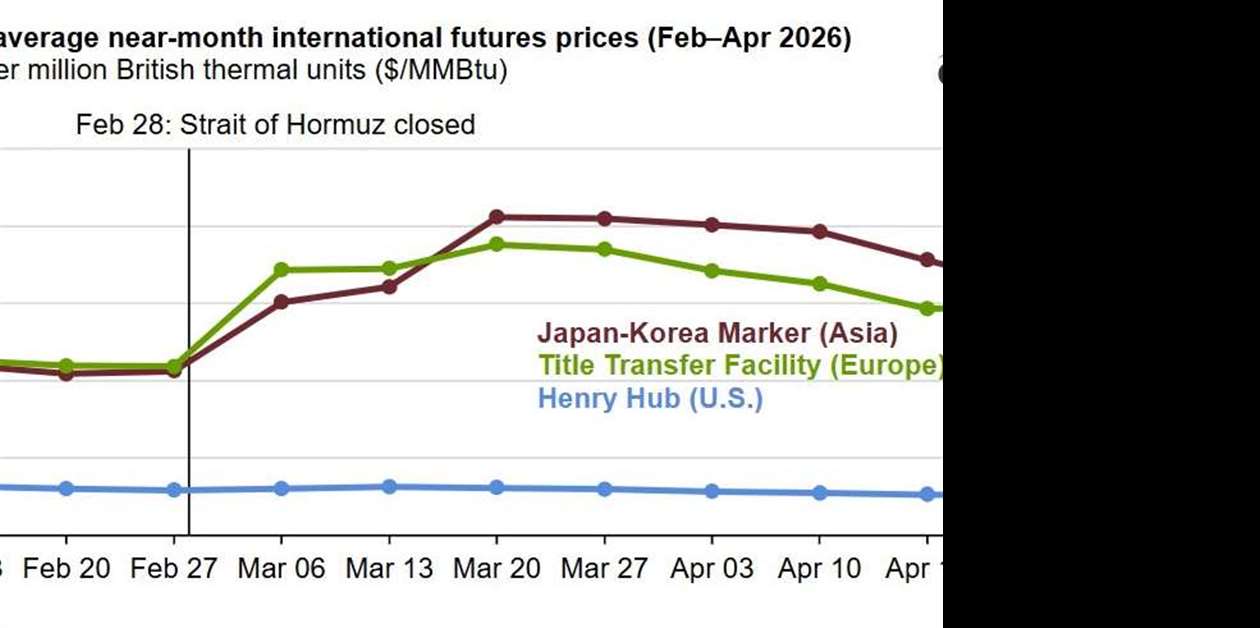

Closure of the Strait of Hormuz disrupted a substantial share of Qatari LNG flows and led QatarEnergy to declare force majeure, driving a sharp divergence in Europe/Asia spot gas pricing versus the U.S. market. The article cites no laden LNG tankers crossing the strait between March 1 and April 24 and shows TTF and JKM front‑month futures moving materially higher. Watch whether force majeure is lifted and how quickly cargoes are rerouted or replaced, because that timing determines short‑term pass‑through and mobilization pressure for service contracts

Buyer takeaway

Treat this as an operationally real driver of spot‑price volatility and logistics risk for LTSA and spare deliveries; act on contract language and carrier contingencies

Cost / money

Direct upward pressure on any LTSA or service fees that include fuel or spot‑indexed pass‑throughs; buyers without caps or hedges face increased operating expense risk

Supplier / commercial

Suppliers may shorten quote validity and press for pass‑throughs or premium scheduling charges; some may invoke force majeure on logistics‑dependent obligations

Safety / operations

Rerouted cargoes and constrained lifts increase the chance of delayed spares and compressed commissioning windows, elevating outage and integration risk

What to watch

Monitor duration of declared force majeure, storage fill levels in Europe/Asia, and supplier invocation of logistics clauses

Key facts

- No laden LNG tankers crossed the strait between March 1 and April 24

- Disruption estimated at roughly 10 Bcf/d of traded LNG tied to Ras Laffan

- European and Asian front‑month futures moved sharply higher through late April

Source excerpts

The resulting supply shock has forced buyers in Asia and Europe to compete more aggressively for available spot cargoes. QatarEnergy declared force majeure on March 4, leaving Asian importers — which typically take more than 80% of Qatari LNG volumes — scrambling to replace contracted deliveries

S. prices relatively insulated due to limited near-term export flexibility and ample domestic supply

QatarEnergy declared force majeure on March 4, leaving Asian importers — which typically take more than 80% of Qatari LNG volumes — scrambling to replace contracted deliveries