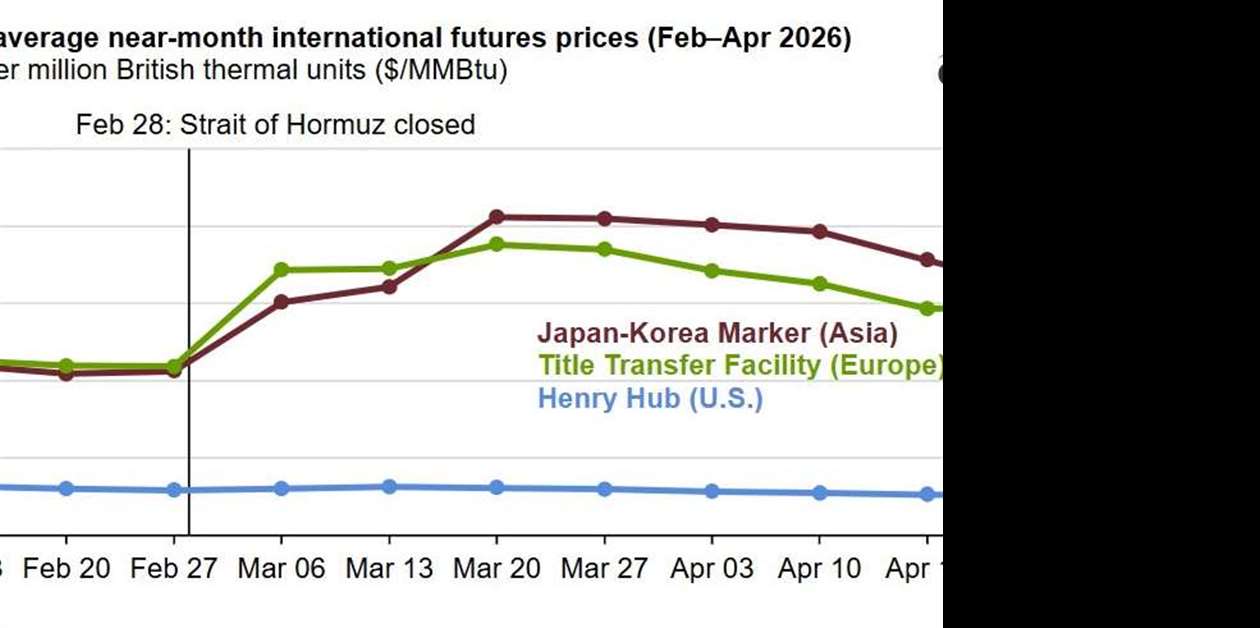

Europe, Asia LNG prices climb on Hormuz closure

What happened

A closure of the Strait of Hormuz and a Qatar force majeure have sidelined a significant portion of traded LNG, lifting European and Asian spot benchmarks while US prices stayed relatively insulated. This is operationally real: the disruption removed a material share of cargoes and forced buyers to seek replacements and reroutes, affecting timing and freight. Watch force majeure extensions, cargo tracking, and storage refill dynamics that will directly affect shipping and spare logistics

Buyer takeaway

Treat this as a concrete supply shock that can trigger allocation and premium freight costs for buyers without reserved capacity

Cost / money

Directional increase in spot LNG and freight premiums is likely for buyers needing near-term cargoes or ad-hoc shipping

Supplier / commercial

Carriers and suppliers will have leverage to shorten quote validity and require reservation commitments while disruption persists

Safety / operations

Rerouted voyages and compressed transits raise scheduling risk for commissioning crews and spare delivery windows

What to watch

Monitor force majeure status and cargo tracking; extended disruptions justify moving toward secured bookings and staged spares

Key facts

- Disruption sidelined more than 10 Bcf/d of traded LNG

- Europe/Asia spot benchmarks rose materially while US prices were insulated

- QatarEnergy declared force majeure in early March

Source excerpts

Export terminal utilization reached 94% of DOE-approved capacity in March, up from 91% in February, leaving little room for a material near-term increase in exports

QatarEnergy declared force majeure on March 4, leaving Asian importers — which typically take more than 80% of Qatari LNG volumes — scrambling to replace contracted deliveries

The resulting supply shock has forced buyers in Asia and Europe to compete more aggressively for available spot cargoes. QatarEnergy declared force majeure on March 4, leaving Asian importers — which typically take more than 80% of Qatari LNG volumes — scrambling to replace contracted deliveries