Australian offshore production license paving the way for first gas in 2028

What happened

Amplitude Energy received a production licence (VIC/L37) for the Annie field, moving the asset from exploration to a permitted development path with first gas planned for 2028. This makes development activities actionable in Australia and increases demand for wells, subsea tie‑ins and local fabrication; watch procurement steps for tendering and long‑lead orders

Buyer takeaway

Treat the licence as a real near‑term demand signal that will generate tenders for wells and subsea works rather than a distant exploration outcome

Cost / money

Development budgets will shift from optional exploration lines to committed mobilisation and long‑lead procurement spend, tightening buyer negotiation leverage on pricing windows

Supplier / commercial

Local and regional suppliers can press for conditional holds and mobilisation deposit clauses as the project moves to execution

Safety / operations

Development schedules require documented HSE readiness and equipment verification ahead of mobilisations to avoid late non‑conformances

What to watch

Watch tender timelines, long‑lead equipment orders, and any local content constraints that could delay integration to existing Otway infrastructure

Key facts

- Production licence awarded: VIC/L37 for the Annie field

- Project positioned to supply east coast domestic gas

- First gas planned for 2028

Source excerpts

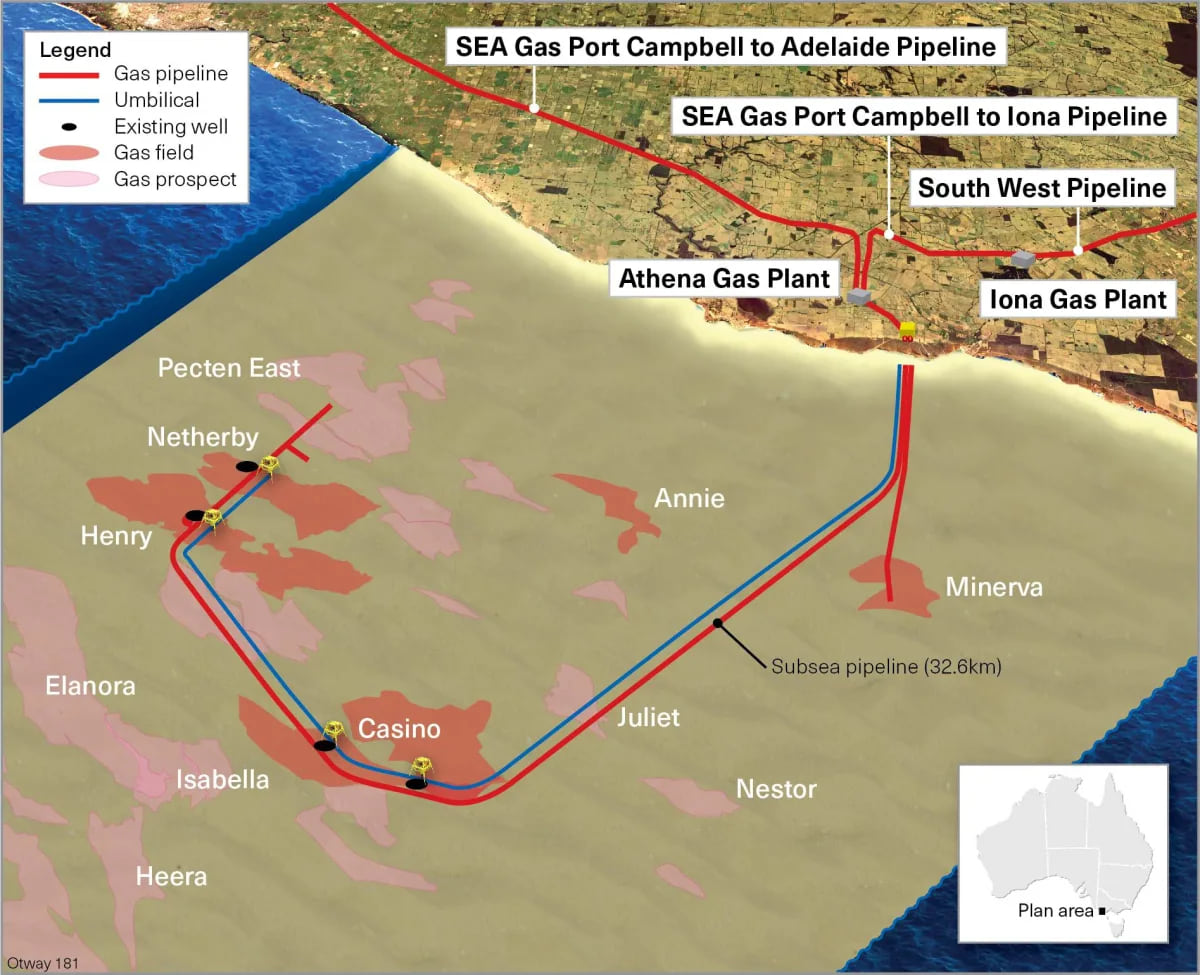

Otway Basin assets; Source: Amplitude Energy Amplitude Energy has received a production licence, VIC/L37, which covers the Annie field that was first discovered in 2019

“Timely approvals and regulatory certainty for oil & gas projects remain critical given the length of investment cycle required

Otway Basin assets; Source: Amplitude Energy Amplitude Energy has received a production licence, VIC/L37, which covers the Annie field that was first discovered in 2019. Thanks to this, the firm can move forward with field development activities, with the first gas planned for 2028