$30 billion mega gas project set to enrich Australia’s countrywide GDP by $98.7 billion

What happened

Woodside published an economic impact assessment tied to a concept‑phase Browse/North‑West Shelf (NWS) extension that highlights the project’s large capital scale and long‑term regional economic benefit. The project remains in concept definition with ongoing activities to support FEED entry; the developer has secured environmental approval at state level, which keeps the project a material future demand signal for WA fabrication, marine and construction suppliers. Watch FEED entry and FEED‑related supplier slot commitments as the next concrete timing signal for mobilisation demand

Buyer takeaway

Treat the NWS concept progress as a multi‑year capacity driver in WA — mobilisations and yard slots will be reprioritised by suppliers toward this scale of work

Cost / money

Directional upward pressure on mobilisation premiums, lead times and contractor pass‑through clauses as suppliers reallocate capacity to higher‑value projects

Supplier / commercial

Suppliers will shorten quote windows and seek mobilisation deposits or earlier milestone billing where they can; relationship frameworks and early slot commitments become stronger negotiation levers

Safety / operations

Clustered site activity increases SIMOPS risk; procurement should require staged handover and independent verification to protect schedule and HSE

What to watch

Watch FEED entry dates and any supplier communications on slot reservations or deposit terms as an early indicator of mobilisation‑pricing shifts

Key facts

- Project in concept definition phase with activities supporting FEED entry

- Capital expenditure estimated in the report at approximately $25–$30 billion

- Reported large economy‑wide employment and tax uplift expectations

Source excerpts

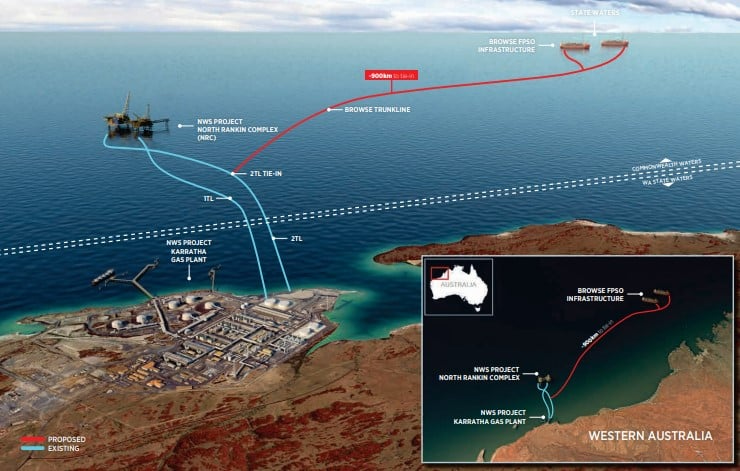

Browse to North-West Shelf project development concept; Source: Woodside After Woodside obtained environmental approval for the North West Shelf (NWS) project extension from the Western Australian government, restarting the federal environmental approvals process, the green light was perceived to be the key to advancing the firm’s Browse gas project and extending the Karratha gas plant’s life to 2070. This project is currently in the concept definition phase, and key activities continue in support of progress

The Australian operator has now released an economic impact assessment by Deloitte Access Economics, which estimates the Browse to NWS project could contribute a long-term uplift of around A$147 billion ($102

This project is currently in the concept definition phase, and key activities continue in support of progress towards front-end engineering and design (FEED) entry