Valaris gains more work for drillship and multiple jackup rigs

What happened

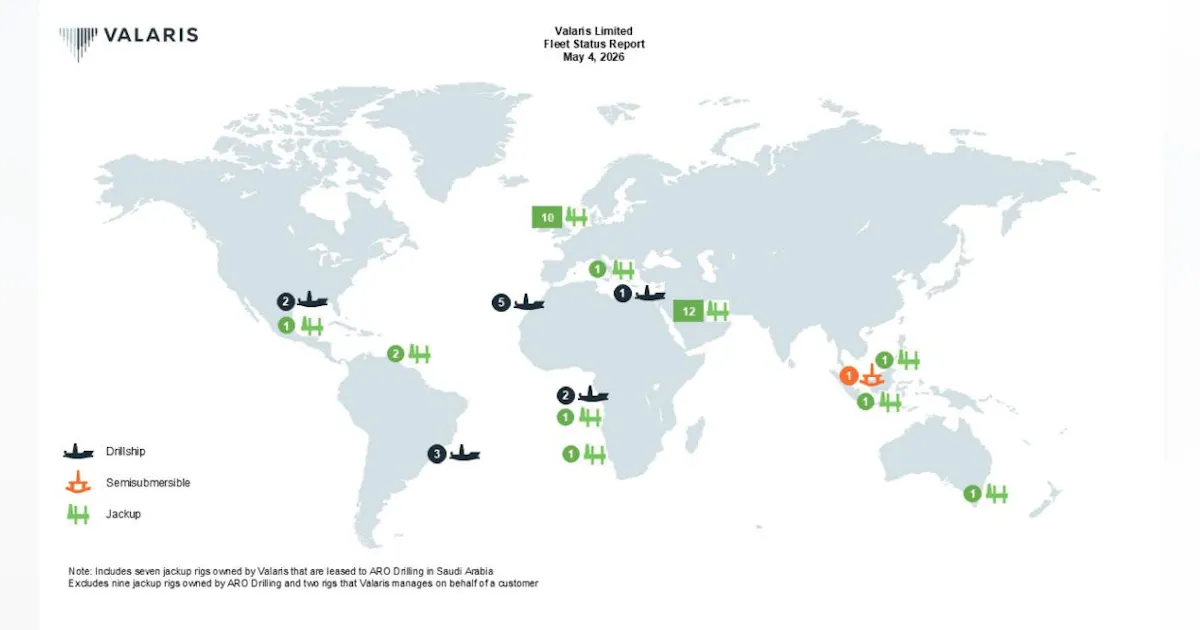

Valaris announced new contracts and multiple contract extensions that substantially increase its backlog and cover drillship and jackup programs across regions. The notices also list shipyard delays and at least one suspended operation, which affects timing and near-term availability. Procurement should watch extension start dates and shipyard completion timing to assess mobilisation and substitution risk

Buyer takeaway

Treat the Valaris backlog changes as a concrete capacity signal — rigs and accommodation days are moving off the open market and suppliers will press for deposits and shorter quote windows

Cost / money

Directional impact toward higher near-term mobilisation and holding costs because extended bookings reduce negotiable supply and increase substitution premiums

Supplier / commercial

Contracted drillship/jackup operators gain leverage to shorten quote validity and demand deposits; expect accelerated pushback on pass-through caps

Safety / operations

Compressed mobilisation timing and extended campaign lengths increase complexity in crew rotations and HSE interface points; confirm readiness windows early

What to watch

Watch start and resumption dates and shipyard completion notes — they determine whether substitution or chartering becomes necessary

Key facts

- Combined contract awards and extensions valued at about $560 million in disclosures

- Drillship extension of the VALARIS DS-4 and multiple jackup extensions across regions

- Shipyard delays announced for some units and at least one rig suspension reported

Source excerpts

The company also revealed that completion of planned shipyard projects for the VALARIS 116 and VALARIS 250 has been delayed, with bareboat charters for the rigs set to resume now and during the third quarter. Operations for VALARIS 110, under contract to NOC offshore Qatar, have been suspended since early March

Valaris has secured new contracts and contract extensions with a combined value of about $560 million, lifting the company’s total backlog to $4

The company also revealed that completion of planned shipyard projects for the VALARIS 116 and VALARIS 250 has been delayed, with bareboat charters for the rigs set to resume now and during the third quarter